library(ISLR)해당 자료는 전북대학교 이영미 교수님 2023응용통계학 자료임

Data

Credit Card Default Data :

A simulated data set containing information on ten thousand customers. The aim here is to predict which customers will default on their credit card debt.

default : A factor with levels No and Yes indicating whether the customer defaulted on their debt

student : A factor with levels No and Yes indicating whether the customer is a student

balance : The average balance that the customer has remaining on their credit card after making their monthly payment

income : Income of customer

head(Default)| default | student | balance | income | |

|---|---|---|---|---|

| <fct> | <fct> | <dbl> | <dbl> | |

| 1 | No | No | 729.5265 | 44361.625 |

| 2 | No | Yes | 817.1804 | 12106.135 |

| 3 | No | No | 1073.5492 | 31767.139 |

| 4 | No | No | 529.2506 | 35704.494 |

| 5 | No | No | 785.6559 | 38463.496 |

| 6 | No | Yes | 919.5885 | 7491.559 |

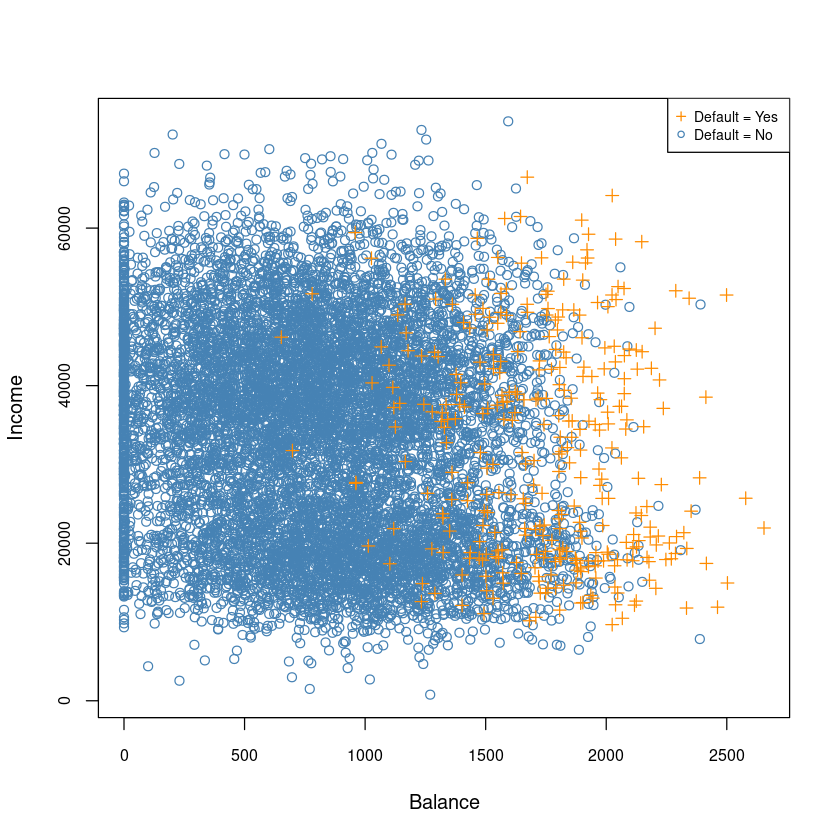

plot(Default$balance, Default$income,type='n',

xlab='Balance',

ylab = 'Income',

cex.axis = 0.8)

points(Default[Default$default=='No',]$balance,

Default[Default$default=='No',]$income,col='steelblue')

points(Default[Default$default=='Yes',]$balance,

Default[Default$default=='Yes',]$income,col='darkorange', pch=3)

legend("topright", c("Default = Yes", "Default = No"),

col=c('darkorange', 'steelblue'),

pch = c(3,1),

# bty = "n",

cex=0.7)

- Balance와 Income은 상관관계가 없어 보인다.

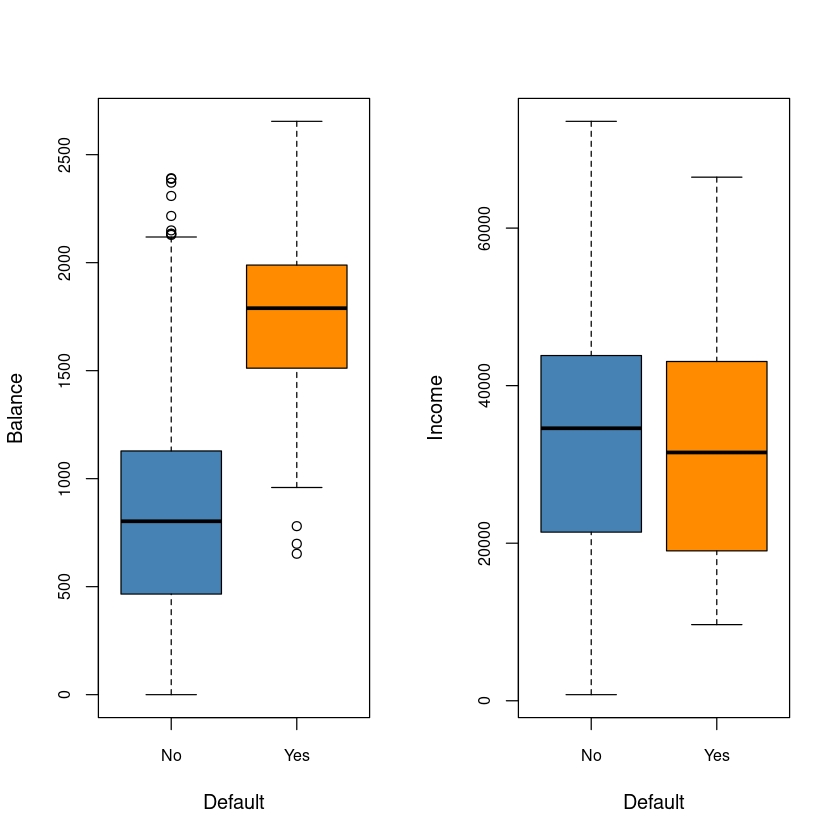

par(mfrow=c(1,2))

boxplot(balance~default, data=Default,cex.axis = 0.8,

xlab = 'Default', ylab='Balance', col=c('steelblue', 'darkorange'))

boxplot(income~default, data=Default,cex.axis = 0.8,

xlab = 'Default', ylab='Income', col=c('steelblue', 'darkorange'))

- income은 default와는 관계가 없어보인다.

Logistic regression

ordinary linear model : \(y = β_0 + β_1x + ϵ\)

Logistic Regression model

\[ log \left( \dfrac{p(y=1|x)}{p(y=0|x)} \right) = log \left( \dfrac{p(x)}{1-p(x)} \right) = \beta_0 + \beta_1 x\]

- 단순선형회귀모형

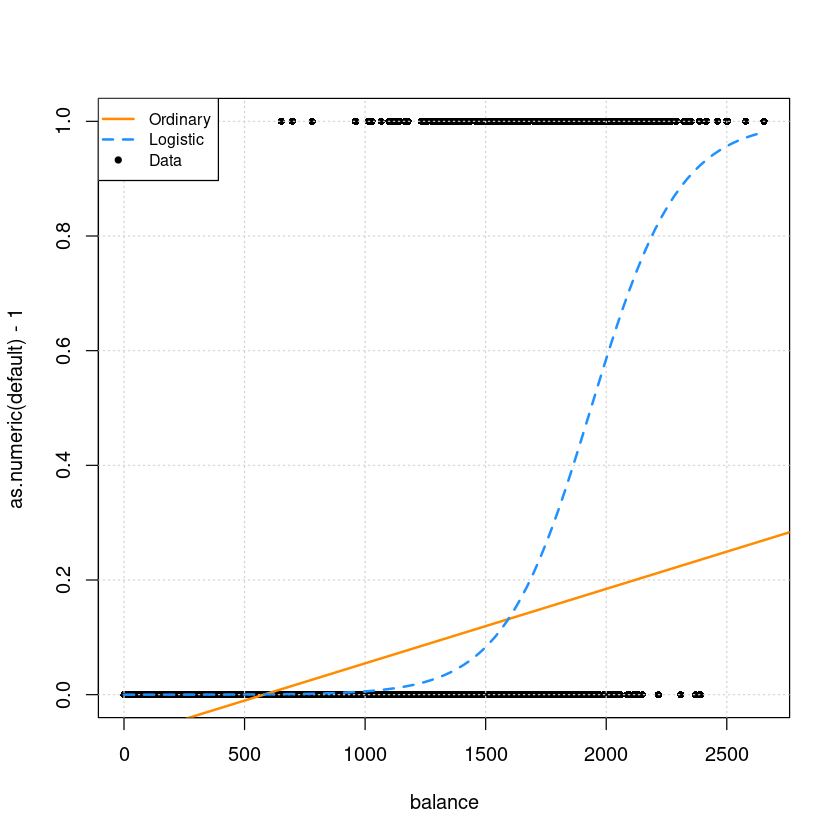

lm.fits <- lm(as.numeric(default)-1 ~ balance,data = Default)

summary(lm.fits)

Call:

lm(formula = as.numeric(default) - 1 ~ balance, data = Default)

Residuals:

Min 1Q Median 3Q Max

-0.23533 -0.06939 -0.02628 0.02004 0.99046

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -7.519e-02 3.354e-03 -22.42 <2e-16 ***

balance 1.299e-04 3.475e-06 37.37 <2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 0.1681 on 9998 degrees of freedom

Multiple R-squared: 0.1226, Adjusted R-squared: 0.1225

F-statistic: 1397 on 1 and 9998 DF, p-value: < 2.2e-16y가 0 또는 1의 값인데 numeric으로 하면 1,2로 나와서 -1로 빼줌

모형 유의하지만 \(R^2\)값이 굉장히 작다.

- GLM(일반화 선형모형) 안에 있는 Logistic Regression

- family=binomial 쓰면 logistic 회귀모형

glm.fits <- glm(default ~ balance,

data = Default, family = binomial) # logistic regression

summary(glm.fits)

Call:

glm(formula = default ~ balance, family = binomial, data = Default)

Deviance Residuals:

Min 1Q Median 3Q Max

-2.2697 -0.1465 -0.0589 -0.0221 3.7589

Coefficients:

Estimate Std. Error z value Pr(>|z|)

(Intercept) -1.065e+01 3.612e-01 -29.49 <2e-16 ***

balance 5.499e-03 2.204e-04 24.95 <2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

(Dispersion parameter for binomial family taken to be 1)

Null deviance: 2920.6 on 9999 degrees of freedom

Residual deviance: 1596.5 on 9998 degrees of freedom

AIC: 1600.5

Number of Fisher Scoring iterations: 8Null deviance: 설명변수가 없는것Residual deviance: 설명변수가 있는것. 값이 크면 모형적합이 덜 된것. 값이 작아야 모형적합이 잘 된 것!.AIC는 작을수록 조흥ㅁ

z value= \(\dfrac{\hat \beta_1}{s.e(\hat \beta_1)}\) ~H0 \(N\)

head(fitted(glm.fits))- 1

- 0.00130567967421633

- 2

- 0.00211259491358475

- 3

- 0.00859474053900645

- 4

- 0.000434436819304936

- 5

- 0.00177695737814425

- 6

- 0.00370415282222879

\(log \dfrac{p(x)}{1-p(x)}=\beta_0+\beta_1x\) : logit… link function

\(p(x) = \dfrac{e^{\beta_0+\beta_1x}}{1+e^{\beta_0+\beta_1x}}\) = \(P(y=1|x)\)

par(mfrow=c(1,1))

plot(as.numeric(default)-1 ~ balance,data = Default, pch=16, cex=0.8)

grid()

abline(lm.fits, col='darkorange', lwd=2)

curve(predict(glm.fits,data.frame(balance=x), type = "response"),

add = TRUE, col = "dodgerblue", lty = 2, lwd=2)

legend("topleft", c("Ordinary", "Logistic", "Data"), lty = c(1, 2, 0),

pch = c(NA, NA, 20), lwd = 2, col = c("darkorange", "dodgerblue", "black"), cex=0.8)

Predict

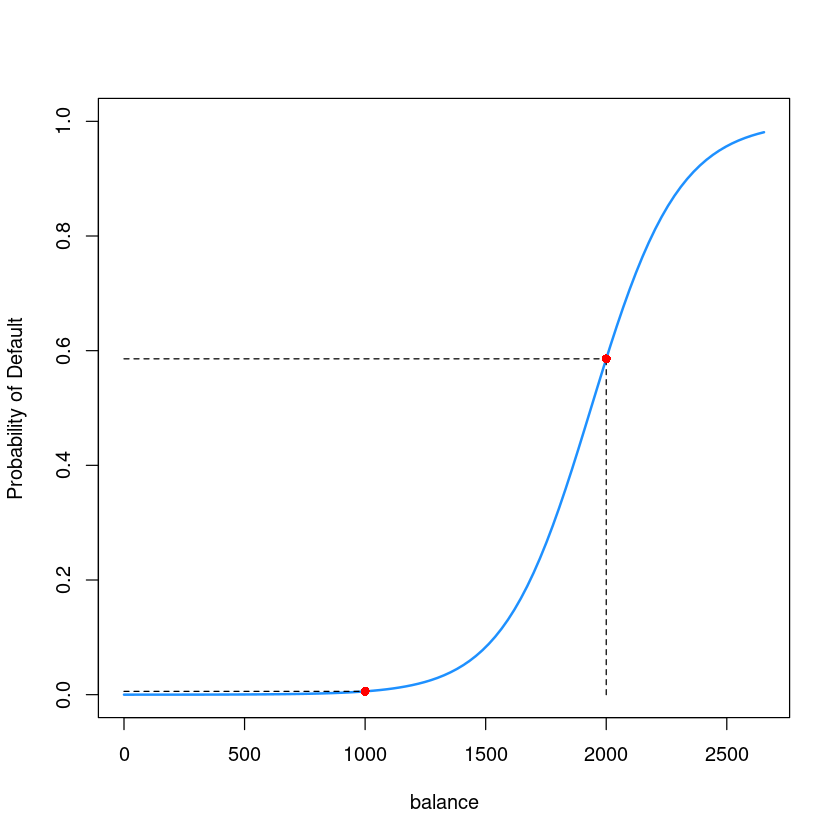

predict(glm.fits, data.frame(balance=2000)) #type='link' : default

1: 0.346503247961301

- 위의 값은 \(log\dfrac{p(x)}{1-p(x)}\)값

predict(glm.fits, data.frame(balance=2000), type='response')

1: 0.585769369615381

type = 'response'해야 \(p(x)\)값을 구할 수 있음.

y_2000 <- predict(glm.fits, newdata = data.frame(balance=2000), type='response');y_2000

1: 0.585769369615381

- $P(Default = “Yes” | Balance = 2000) = 0.585769369615381 $

y_1000 <- predict(glm.fits, newdata = data.frame(balance=1000), type='response');y_1000

1: 0.00575214508582045

par(mfrow=c(1,1))

plot(as.numeric(default)-1 ~ balance,data = Default,

ylab = "Probability of Default" ,

pch=16, cex=0.8, type='n')

curve(predict(glm.fits,data.frame(balance=x), type = "response"),

add = TRUE, col = "dodgerblue", lwd=2)

lines(c(0, 2000),c(y_2000, y_2000), lty=2)

lines(c(2000, 2000),c(0, y_2000), lty=2)

points(2000, y_2000, col='red', cex=1, pch=16)

lines(c(0, 1000),c(y_1000, y_1000), lty=2)

lines(c(1000, 1000),c(0, y_1000), lty=2)

points(1000, y_1000, col='red', cex=1, pch=16)

Confidence Interval

summary(glm.fits)

Call:

glm(formula = default ~ balance, family = binomial, data = Default)

Deviance Residuals:

Min 1Q Median 3Q Max

-2.2697 -0.1465 -0.0589 -0.0221 3.7589

Coefficients:

Estimate Std. Error z value Pr(>|z|)

(Intercept) -1.065e+01 3.612e-01 -29.49 <2e-16 ***

balance 5.499e-03 2.204e-04 24.95 <2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

(Dispersion parameter for binomial family taken to be 1)

Null deviance: 2920.6 on 9999 degrees of freedom

Residual deviance: 1596.5 on 9998 degrees of freedom

AIC: 1600.5

Number of Fisher Scoring iterations: 8- 95% CI : \(\hat \beta_1 \pm z_{0.025} s.e(\hat \beta_1)\)

- 방법1

confint(glm.fits, level = 0.95)Waiting for profiling to be done...

| 2.5 % | 97.5 % | |

|---|---|---|

| (Intercept) | -11.383288936 | -9.966565064 |

| balance | 0.005078926 | 0.005943365 |

- 방법2

summary(glm.fits)$coef| Estimate | Std. Error | z value | Pr(>|z|) | |

|---|---|---|---|---|

| (Intercept) | -10.651330614 | 0.3611573721 | -29.49221 | 3.623124e-191 |

| balance | 0.005498917 | 0.0002203702 | 24.95309 | 1.976602e-137 |

summary(glm.fits)$coef[2,1] + qnorm(0.975)*summary(glm.fits)$coef[2,2]

0.00593083451913757

summary(glm.fits)$coef[2,1] - qnorm(0.975)*summary(glm.fits)$coef[2,2]

0.00506699934268553

Classification

로지스틱은 분류모형에 해당

\(P(y=1|x) > 0.5 \rightarrow\) Default \(\hat y=1\)

\(P(y=1|x) \leq 0.5 \rightarrow\) Default \(\hat y=0\)

로 바꾸면 classification이 된다. 그럼 저렇게 0.5와 같은 기준값 (\(cut-off\))를 뭘로 정할까?

fitted.default.prob <- predict(glm.fits, type='response')

head(fitted.default.prob)- 1

- 0.00130567967421633

- 2

- 0.00211259491358475

- 3

- 0.00859474053900645

- 4

- 0.000434436819304936

- 5

- 0.00177695737814425

- 6

- 0.00370415282222879

class.default <- ifelse(fitted.default.prob > 0.5, 'Yes', "No")

head(class.default)- 1

- 'No'

- 2

- 'No'

- 3

- 'No'

- 4

- 'No'

- 5

- 'No'

- 6

- 'No'

table(Default$default, class.default) class.default

No Yes

No 9625 42

Yes 233 100왼쪽이 실제!

정분류율은 0.9725

class.default <- ifelse(fitted.default.prob > 0.3, 'Yes', "No")

head(class.default)- 1

- 'No'

- 2

- 'No'

- 3

- 'No'

- 4

- 'No'

- 5

- 'No'

- 6

- 'No'

table(Default$default, class.default) class.default

No Yes

No 9520 147

Yes 166 167